What Factors Should I Consider When Choosing a Health Insurance Provider for My Business?

Selecting a health insurance provider for your business is a critical decision that can significantly impact your employees’ well-being and your company’s financial health. Understanding the various factors involved in this choice is essential for ensuring that you provide adequate coverage while managing costs effectively. This article will guide you through the key considerations when choosing a health insurance provider, including the types of plans available, coverage options, cost factors, and compliance requirements. By the end, you will have a comprehensive understanding of how to navigate the complexities of health insurance for your business. For businesses operating in Michigan, consulting a comprehensive Michigan employer health insurance guide can provide valuable localized insights.

About the Author

About the Author: Sunny Connolly, Licensed Employee Benefits Consultant at CFH Insurance Consultants. With over 30 years of experience serving Michigan’s mid-market employers, Sunny specializes in strategic cost optimization and innovative plan design. He is NAHU certified and has helped hundreds of Michigan businesses achieve sustainable benefits growth.

Reviewed by: Michael Thompson, CEBS (Certified Employee Benefit Specialist) – Independent benefits compliance auditor with 20+ years of experience reviewing Michigan employer health plans.

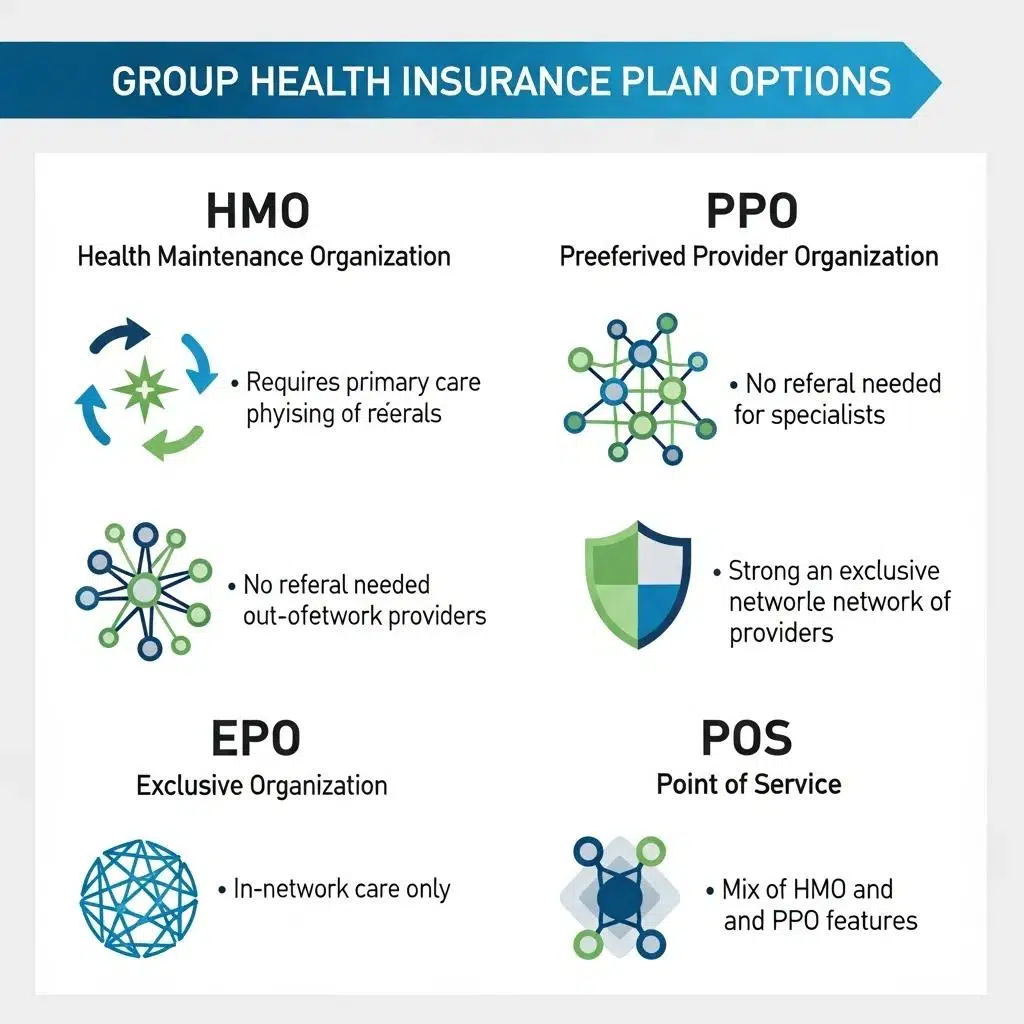

What Are the Key Types of Group Health Insurance Plans for Businesses?

Group health insurance plans are designed to provide coverage for employees under a single policy, which can be more cost-effective than individual plans. The primary types of group health insurance plans include:

- Health Maintenance Organizations (HMOs): These plans require members to choose a primary care physician and get referrals for specialist services. They often have lower premiums but less flexibility in choosing providers.

- Preferred Provider Organizations (PPOs): PPOs offer more flexibility in choosing healthcare providers and do not require referrals for specialists. However, they typically come with higher premiums and out-of-pocket costs.

- Exclusive Provider Organizations (EPOs): EPOs combine features of HMOs and PPOs, offering a network of providers without requiring referrals but limiting coverage to in-network services.

- Point of Service (POS) Plans: These plans allow members to choose between HMO and PPO options at the time of service, providing a balance of flexibility and cost.

Understanding these types of plans can help businesses select the most suitable option based on their employee needs and budget.

Research highlights how these managed care organizations, like HMOs and PPOs, have evolved to help businesses control healthcare costs.

HMO & PPO Health Plans for Business Cost Control

As a result, health maintenance organizations (HMOs) and other forms of prepaid health care were widely adopted with the aim of reducing health-care costs. The evolution, restructuring, and influence of managed care organizations in the delivery of health care peaked in the 1980s and 1990s.

Breaking down health care insurance from HMO to PPO and beyond, 2013

How Do Group Health Insurance Plans Differ from Individual Plans?

Group health insurance plans differ significantly from individual plans in several key areas.

- Cost: Group plans generally offer lower premiums due to the risk being spread across a larger pool of individuals. Employers often contribute to the premium costs, making it more affordable for employees.

- Coverage: Group plans typically provide more comprehensive coverage options, including preventive care, which may not be as extensive in individual plans.

- Eligibility: Group plans are available to all employees, whereas individual plans require individuals to apply and may involve medical underwriting, which can lead to higher costs for those with pre-existing conditions.

- Tax Benefits: Employers can often deduct the cost of group health insurance premiums as a business expense, providing additional financial incentives compared to individual plans.

These differences highlight the advantages of group health insurance for businesses looking to provide comprehensive coverage to their employees.

What Coverage Options Are Included in Typical Group Health Insurance Plans?

Typical group health insurance plans include a variety of coverage options designed to meet the diverse needs of employees. Common coverage options include:

- Preventive Care: Services such as annual check-ups, vaccinations, and screenings that help detect health issues early.

- Hospitalization: Coverage for inpatient services, including surgeries and overnight stays in hospitals.

- Prescription Drug Coverage: Assistance with the cost of medications, which can significantly reduce out-of-pocket expenses for employees.

- Mental Health Services: Access to counseling and therapy services, which are increasingly recognized as essential for overall health.

- Rehabilitative Services: Coverage for physical therapy and other rehabilitative services that help employees recover from injuries or surgeries.

These coverage options are crucial for ensuring that employees have access to the healthcare services they need, promoting a healthier workforce.

This table illustrates the essential coverage options typically included in group health insurance plans, emphasizing their importance in promoting employee health and well-being.

Which Factors Affect the Cost and Value of Business Health Insurance Plans?

Several factors influence the cost and value of business health insurance plans, making it essential for employers to consider these elements when selecting a provider.

- Provider Reputation: The reputation of the insurance provider can impact both the quality of care employees receive and the overall satisfaction with the plan. For businesses in Michigan, researching the best group health insurance providers in Michigan can be particularly beneficial.

- Financial Stability: A provider’s financial health is crucial for ensuring they can meet their obligations to policyholders, especially during times of high claims.

- Customization Options: The ability to tailor plans to meet the specific needs of employees can enhance the value of the insurance offered, making it more attractive to potential hires.

- Claims History: A provider’s claims history can indicate how efficiently they handle claims and the likelihood of future rate increases.

By evaluating these factors, businesses can make informed decisions that balance cost with the quality of care provided. Exploring affordable options for mid-size employers can also help manage expenses effectively.

Indeed, the ongoing challenge of rising healthcare costs makes the careful selection of a provider based on specific criteria even more crucial for businesses.

Criteria for Choosing Business Health Insurance Providers

Expenses related to employee’s health benefit packages are rising. Hence, organisations are looking for complementary health financing arrangements to provide more financial protection for employees. This study aims to develop criteria to choose the most appropriate complementary health insurance company based on the experience of a large organisation in Iran.

Criteria for the selection of complementary private health insurance: the experience of a large organisation in Iran, M Alipouri Sakha, 2022

How Do Provider Networks Influence Health Insurance Costs and Access?

Provider networks play a significant role in determining health insurance costs and access to care.

- Network Size and Quality: Larger networks typically offer more choices for employees, which can enhance satisfaction. However, plans with extensive networks may come with higher premiums.

- Plan Types and Restrictions: Different plans have varying levels of access to out-of-network providers. Plans that require using in-network providers can help control costs but may limit employee choice.

- Cost Implications: The structure of the provider network can affect out-of-pocket costs for employees, including deductibles, copayments, and coinsurance.

Understanding how provider networks operate is essential for businesses to ensure that their employees have access to necessary healthcare services while managing costs effectively.

For example, a 150-employee manufacturing company in Grand Rapids recently switched carriers after discovering that their previous provider’s network didn’t include Spectrum Health’s main facilities, forcing employees to drive to Lansing for specialized care. After CFH Insurance Consultants conducted a network analysis, we identified a carrier with comprehensive West Michigan coverage, reducing employee out-of-network costs by 40% and improving satisfaction scores by 35 points.

What Role Does Plan Coverage and Benefits Play in Cost Management?

The coverage and benefits provided by a health insurance plan are critical in managing overall costs for both employers and employees.

- Cost Structure of Different Plans: Plans with higher premiums may offer lower out-of-pocket costs, while those with lower premiums might result in higher costs when employees seek care. Considering customizable plan options can help tailor coverage to balance cost and benefits.

- Employee Demographics: The age and health status of employees can influence the type of coverage needed, impacting overall costs. Younger, healthier workforces may benefit from high-deductible plans, while older employees may require more comprehensive coverage.

- Claims History: A company’s claims history can affect future premiums. Plans that effectively manage claims can help keep costs down over time.

By carefully considering the relationship between coverage, benefits, and costs, businesses can select plans that provide value while managing expenses.

How Can Alternative Reimbursement Arrangements Like QSEHRA and ICHRA Benefit Employers?

Alternative reimbursement arrangements, such as Qualified Small Employer Health Reimbursement Arrangements (QSEHRA) and Individual Coverage Health Reimbursement Arrangements (ICHRA), offer unique benefits for employers.

- Cost Savings: These arrangements allow employers to reimburse employees for individual health insurance premiums and out-of-pocket expenses, potentially reducing overall costs compared to traditional group plans.

- Employee Satisfaction: By providing employees with the flexibility to choose their own plans, employers can enhance satisfaction and retention.

- Regulatory Compliance: QSEHRA and ICHRA are designed to comply with federal regulations, including ACA Section 1557, making them a viable option for small businesses looking to offer health benefits.

What Are QSEHRA and ICHRA and How Do They Work?

QSEHRA and ICHRA are innovative health reimbursement arrangements that allow employers to reimburse employees for health insurance costs.

- QSEHRA: Designed for small employers, QSEHRA allows businesses to reimburse employees for individual health insurance premiums and qualified medical expenses up to a specified limit. This arrangement is tax-free for both employers and employees.

- ICHRA: This option is available to employers of any size and allows for more flexibility in reimbursement amounts and eligibility criteria. Employers can set different reimbursement levels based on employee classes, such as full-time, part-time, or seasonal workers.

Both arrangements provide a way for employers to offer health benefits while controlling costs and complying with regulations.

How Do These Arrangements Compare to Traditional Group Health Insurance?

When comparing QSEHRA and ICHRA to traditional group health insurance, several key differences emerge.

- Flexibility: QSEHRA and ICHRA allow employees to choose their own health plans, providing greater flexibility than traditional group plans, which often have limited options.

- Cost Control: Employers can set reimbursement limits, making it easier to manage costs compared to the fixed premiums associated with group plans.

- Employee Choice: These arrangements empower employees to select plans that best meet their individual needs, which can lead to higher satisfaction and better health outcomes.

Understanding these differences can help employers determine the best approach to providing health benefits.

What Complementary Employee Benefits Should Be Considered Alongside Health Insurance?

In addition to health insurance, businesses should consider offering complementary employee benefits that enhance overall compensation packages.

- Dental and Vision Insurance: These benefits are essential for comprehensive employee health and can improve retention rates by addressing additional health needs.

- Disability Insurance: Providing short-term and long-term disability insurance can offer financial security for employees unable to work due to illness or injury.

- Life Insurance: Offering life insurance can provide peace of mind for employees and their families, making it an attractive benefit.

How Do Dental and Vision Insurance Enhance Employee Benefits Packages?

Dental and vision insurance are critical components of a well-rounded benefits package.

- Employee Satisfaction: Access to dental and vision care can significantly enhance employee satisfaction, as these services are often seen as essential.

- Retention Rates: Offering comprehensive benefits, including dental and vision coverage, can improve employee retention by demonstrating a commitment to their overall well-being.

- Health Benefits: Regular dental and vision check-ups can lead to early detection of health issues, contributing to a healthier workforce.

Why Include Disability and Life Insurance in Business Health Plans?

Incorporating disability and life insurance into business health plans is vital for several reasons.

- Financial Security: Disability insurance provides employees with income protection in case of illness or injury, ensuring they can maintain their standard of living.

- Employee Well-Being: Life insurance offers peace of mind, knowing that their families will be financially secure in the event of an untimely death.

- Attracting Talent: Comprehensive benefits packages that include disability and life insurance can help attract top talent in a competitive job market.

What Compliance and Regulatory Requirements Must Employers Meet When Choosing Providers?

Employers must navigate various compliance and regulatory requirements when selecting health insurance providers.

- ACA Compliance: The Affordable Care Act (ACA) mandates that applicable large employers provide health insurance to full-time employees or face penalties. Compliance with ACA Section 1557 ensures non-discrimination in health programs.

- State Regulations: Each state has its own regulations regarding health insurance, which can affect plan offerings and employer responsibilities. For Michigan businesses, understanding Michigan compliance requirements, including Michigan Public Act 350, is essential.

- Non-Discrimination Rules: Employers must ensure that their health insurance plans do not discriminate against employees based on health status or other factors.

Which Employer Health Insurance Requirements Affect Provider Selection?

Several employer health insurance requirements can influence provider selection.

- Documentation and Reporting: Employers must maintain accurate records and reports to demonstrate compliance with ACA and state regulations.

- Penalties for Non-Compliance: Failing to meet health insurance requirements can result in significant penalties, making it crucial for employers to choose compliant providers.

- Provider Reputation: Selecting a provider with a strong reputation for compliance can help mitigate risks associated with regulatory issues.

How Can Employers Ensure Compliance with Health Insurance Laws?

Employers can take several steps to ensure compliance with health insurance laws.

- Conduct Regular Audits: Regular audits of health insurance plans can help identify compliance issues before they become problematic.

- Provide Employee Training: Educating employees about their rights and responsibilities under health insurance laws can promote compliance and reduce misunderstandings.

- Engage Consulting Services: Working with health insurance consultants can provide valuable insights and assistance in navigating complex regulations.

How Can Employers Effectively Manage Costs While Engaging Employees in Health Benefits?

Managing costs while engaging employees in health benefits is a delicate balance that requires strategic planning.

- Cost Control Techniques: Employers can implement cost-sharing strategies, such as high-deductible health plans paired with Health Savings Accounts (HSAs), to manage expenses.

- Employee Engagement Methods: Encouraging employees to participate in wellness programs can lead to healthier lifestyles and lower healthcare costs.

- Impact on Overall Satisfaction: Engaged employees are more likely to appreciate their benefits, leading to higher job satisfaction and retention rates.

What Strategies Help Balance Cost Management and Employee Satisfaction?

Employers can adopt several strategies to balance cost management with employee satisfaction.

- Negotiating with Providers: Establishing strong relationships with insurance providers can lead to better rates and more favorable terms.

- Customization of Benefits: Offering a range of benefits that employees can choose from allows for personalization, which can enhance satisfaction.

- Implementing Wellness Programs: Wellness initiatives can promote healthier behaviors, reducing overall healthcare costs and improving employee morale.

How Do Health Insurance Brokers Support Employers in Plan Selection and Cost Control?

Health insurance brokers play a vital role in assisting employers with plan selection and cost control.

- Expert Guidance: Brokers provide valuable insights into the health insurance market, helping employers navigate complex options.

- Cost Management Strategies: Brokers can identify cost-saving opportunities and negotiate better terms with insurance providers.

- Ongoing Support: Brokers offer continuous support throughout the policy year, ensuring that employers remain compliant and satisfied with their plans. To get started, contact us today. Learn more about how CFH compares to other brokers to make an informed choice.

What Are the Latest Trends and Innovations in Employer Health Insurance Plans?

The landscape of employer health insurance is continually evolving, with new trends and innovations emerging.

- Emerging Coverage Options: Employers are increasingly exploring telehealth services and mental health benefits as essential components of their health plans.

- Cost Management Strategies: Innovative approaches, such as value-based care models, are gaining traction as employers seek to control costs while improving care quality.

- Employee Wellness Initiatives: Programs focused on employee wellness are becoming more prevalent, emphasizing preventive care and overall health improvement.

How Are Telehealth and Mental Health Benefits Changing Business Health Insurance?

Telehealth and mental health benefits are transforming the way businesses approach health insurance.

- Increased Adoption of Telehealth: The convenience of telehealth services allows employees to access care more easily, reducing barriers to treatment.

- Focus on Mental Health Support: Recognizing the importance of mental health, employers are incorporating mental health benefits into their plans, promoting overall well-being.

- Cost Implications: These innovations can lead to cost savings by reducing the need for in-person visits and improving employee health outcomes.

What Is the Impact of Cost Transparency on Employer and Employee Decisions?

Cost transparency is becoming increasingly important in health insurance decisions.

- Cost Management: Providing clear information about costs can help employers make informed decisions about plan offerings and budgeting.

- Employee Attraction and Retention: Transparency in costs can enhance employee trust and satisfaction, making it easier to attract and retain talent.

- Plan Customization: Understanding costs allows employers to tailor benefits to meet the specific needs of their workforce.

How Can Expert Consulting Simplify Choosing the Right Health Insurance Provider?

Expert consulting can significantly simplify the process of selecting the right health insurance provider.

- Customized Benefits Packages: Consultants can help businesses design benefits packages that align with their specific needs and budget.

- Compliance Assistance: Navigating the complexities of health insurance regulations can be daunting, but consultants provide valuable guidance to ensure compliance.

- Ongoing Support: Consultants offer continuous support, helping businesses adapt to changes in the health insurance landscape.

What Services Do Health Insurance Consultants Offer to Businesses?

Health insurance consultants provide a range of services to assist businesses in managing their health benefits.

- Customized Benefits Packages: Consultants work with employers to create tailored benefits packages that meet the unique needs of their workforce.

- Compliance Assistance: They help ensure that businesses remain compliant with health insurance regulations, reducing the risk of penalties.

- Cost Management Strategies: Consultants identify opportunities for cost savings and help negotiate better terms with insurance providers.

How Does Personalized Guidance Improve Provider Selection Outcomes?

Personalized guidance from health insurance consultants can lead to better provider selection outcomes.

- Informed Decision-Making: Consultants provide data-driven insights that empower employers to make informed choices about their health insurance options.

- Enhanced Employee Benefits: By aligning benefits with employee needs, businesses can improve satisfaction and retention.

- Cost Savings: Personalized guidance can uncover cost-saving opportunities that may not be apparent without expert assistance.

To ensure your employees are well taken care of, consider offering employee benefits alongside health insurance.

For small businesses looking for cost-effective solutions, QSEHRA and ICHRA arrangements can be a great alternative to traditional group plans.

Don’t forget the importance of dental and vision coverage as part of your comprehensive benefits package.

Additionally, providing disability and life insurance can offer financial security and peace of mind to your employees.

When making your final decision, be mindful of common selection mistakes to avoid to ensure the best outcomes for your business and employees.

Common Mistakes Made by Michigan Mid-Market Employers and Their Financial Impact

Understanding common mistakes made by Michigan mid-market employers when selecting health insurance plans is crucial to avoid costly errors. Below are three detailed case studies illustrating typical pitfalls, their financial consequences, and how CFH Insurance Consultants help prevent and correct these issues.

1. Pontiac Manufacturing (175 employees): Auto-Renewal Without Market Comparison

Situation: Pontiac Manufacturing auto-renewed their health insurance plan without conducting an annual market comparison in 2026.

Financial Impact: According to the KFF 2026 Survey, 62% of Michigan mid-market employers do not conduct annual market comparisons, resulting in an average overpayment of $1,200 per employee. Pontiac Manufacturing lost approximately $85,000 in the first year due to a 19% higher premium than competitive market rates.

How CFH Helps: CFH implemented a competitive bid process for Pontiac Manufacturing, securing a 19% premium reduction in year one. This process included comprehensive market analysis and negotiation with multiple carriers to ensure the best value.

Prevention Strategies:

- Conduct annual market comparisons before renewing plans.

- Engage brokers or consultants to facilitate competitive bidding.

- Review plan performance and employee satisfaction regularly.

2. Canton Services (130 employees): Choosing Lowest-Cost Plan Without Network Analysis

Situation: Canton Services selected the lowest-cost health insurance plan in 2026 without analyzing the provider network adequacy.

Financial Impact: Mercer 2026 data shows that 34% of Michigan mid-market plans face network adequacy issues. At Canton Services, 40% of employees had no in-network providers within 20 miles, leading to increased out-of-pocket expenses estimated at $800 per affected employee annually.

How CFH Helps: CFH conducted a detailed network analysis and redesigned the plan to improve access to in-network providers. This redesign reduced employee out-of-pocket costs significantly and improved overall satisfaction.

Prevention Strategies:

- Perform thorough network adequacy reviews before plan selection.

- Consider employee geographic distribution when evaluating networks.

- Balance cost savings with access to quality providers.

3. Ann Arbor Retail (200 employees): Wellness Program Implementation Without Legal Review

Situation: Ann Arbor Retail launched a wellness program in 2026 without conducting a legal compliance review.

Financial Impact: The Michigan Department of Insurance and Financial Services (DIFS) 2026 complaint data highlights that compliance violations can result in penalties ranging from $50,000 to $500,000. Ann Arbor Retail faced an EEOC complaint for ADA violations, risking substantial fines and legal costs.

How CFH Helps: CFH redesigned the wellness program to ensure compliance with ADA and other regulations, avoiding penalties and increasing employee participation from 12% to 67%.

Prevention Strategies:

- Conduct legal reviews of wellness programs before implementation.

- Ensure programs comply with ADA, ACA, and other relevant laws.

- Engage compliance experts or consultants to guide program design.

Summary of Financial Impact of Common Mistakes in Michigan Mid-Market Health Plans (2026)

By learning from these examples and data, Michigan mid-market employers can avoid costly mistakes and optimize their health insurance offerings for better financial and employee outcomes.

2026 Michigan Market Data: According to the 2026 Michigan Employer Health Benefits Survey by the Michigan Department of Insurance and Financial Services (DIFS), mid-market employers (50-500 employees) in Michigan pay an average of $8,200 per employee annually for health insurance, with significant variation based on industry and location. Metro Detroit employers average $8,800 per employee, while rural Michigan employers average $7,400. Understanding these benchmarks helps you evaluate whether your current costs are competitive and identify opportunities for savings through strategic plan design.