What Is ICHRA? How Individual Coverage HRAs Work for Small Employers

The Individual Coverage Health Reimbursement Arrangement (ICHRA) is a flexible health benefits solution designed specifically for small employers. It allows businesses to provide employees with a defined contribution towards their health insurance premiums, enabling them to choose plans that best fit their individual needs. Employers looking for an alternative to conventional small business group benefits administration are increasingly turning to ICHRA for its flexibility and cost control. This innovative approach not only enhances employee satisfaction but also offers significant tax advantages for employers. As small businesses navigate the complexities of health benefits, understanding how ICHRA works and its benefits can empower them to make informed decisions. This article will explore the advantages of ICHRA for small employers, compare it with the Qualified Small Employer HRA (QSEHRA), and provide guidance on implementing an ICHRA plan effectively.

This emphasis on employee choice is a foundational element of ICHRA, distinguishing it from traditional group coverage options.

ICHRA for Small Businesses: Employee Choice vs. Group Coverage

ICHRA acknowledged that allowing small businesses to offer employees the choice between group coverage and ICHRA

Put Employees in Control of Health Insurance with “Worker’s Choice ICHRA”, 2025

ICHRA Benefits for Small Employers

ICHRA offers several key advantages for small employers looking to enhance their employee benefits package.

- Flexibility in Employee Benefits: Employers can customize their contributions based on employee needs, allowing for a more tailored approach to health benefits.

- Tax Advantages for Employers: Contributions made to ICHRAs are tax-deductible, providing financial relief for small businesses.

- Attracting and Retaining Talent: Offering ICHRA can make a company more attractive to potential employees, helping to retain top talent in a competitive job market.

The flexibility of ICHRA allows employers to set their contribution limits, which can vary based on employee age and family size. This adaptability ensures that businesses can manage their budgets while still providing valuable health benefits.

These benefits illustrate how ICHRA can serve as a strategic tool for small employers aiming to improve their health benefits offerings.

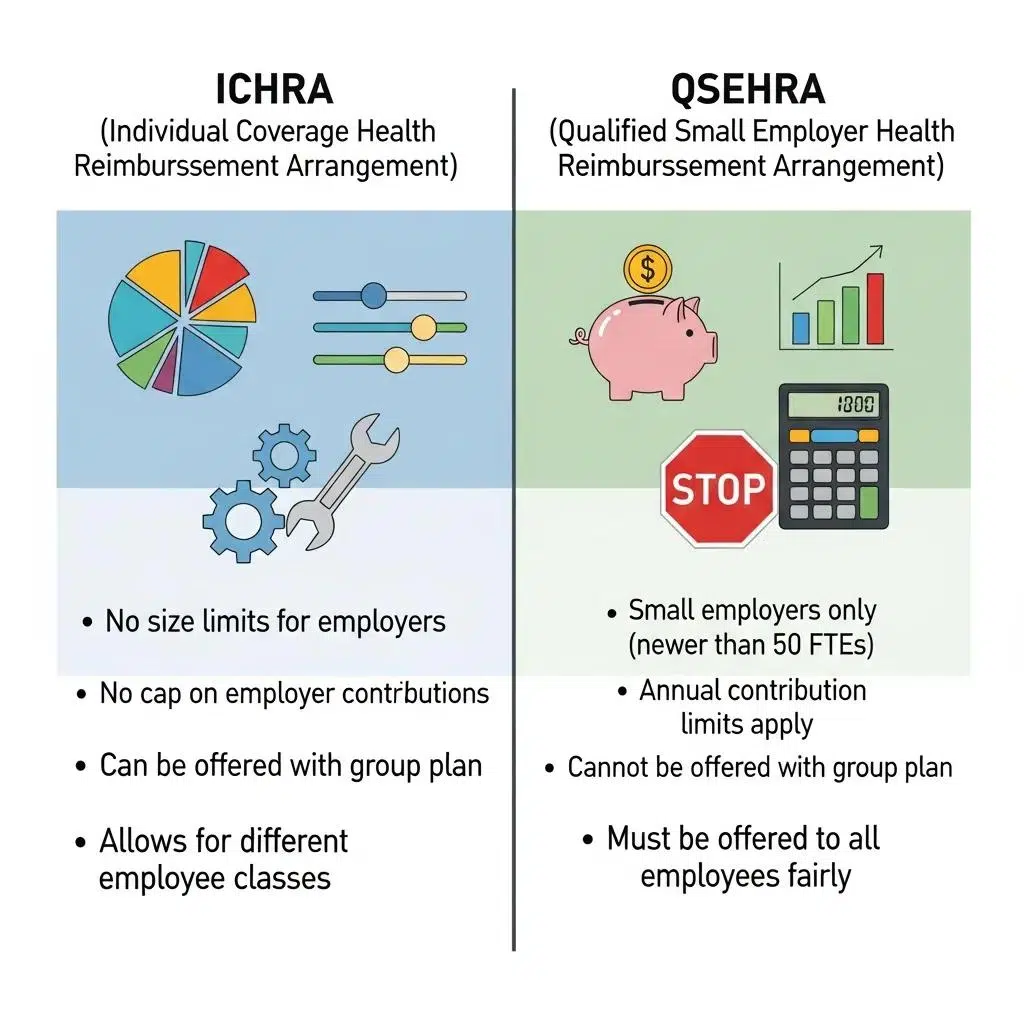

ICHRA vs QSEHRA: Key Differences

When comparing ICHRA to the Qualified Small Employer HRA (QSEHRA), several key differences emerge that can influence a small employer’s choice. Businesses with fewer than 50 employees that do not offer group coverage may qualify for a QSEHRA (Qualified Small Employer HRA), which has lower annual contribution limits but simpler administration.

- Eligibility Criteria Differences: ICHRA allows employers to offer benefits to all employees, while QSEHRA is limited to small employers with fewer than 50 full-time employees.

- Contribution Limits Comparison: ICHRA does not have a set contribution limit, allowing for more flexibility, whereas QSEHRA has specific annual contribution limits set by the IRS.

- Tax Implications: Both options provide tax advantages, but the specifics can vary based on the structure of the plan and the employer’s contributions.

Understanding these differences is crucial for small employers as they evaluate which health reimbursement arrangement best fits their needs.

How to Implement an ICHRA Plan

Implementing an ICHRA plan involves several key steps that small employers should follow to ensure compliance and effectiveness.

- Define Contribution Levels: Employers should determine how much they will contribute to each employee’s health insurance.

- Choose Eligible Employees: Decide which employees will be eligible for the ICHRA, as employers can offer different plans to different groups.

- Communicate with Employees: Clearly explain the ICHRA benefits and how employees can use their reimbursements for health insurance premiums.

For small businesses looking for assistance in setting up an ICHRA plan, consulting services offered by “CFH Insurance Consultants” can provide tailored guidance and support throughout the implementation process.

ICHRA Compliance and IRS Guidelines

Compliance with IRS guidelines is essential for the successful operation of an ICHRA. Employers must adhere to specific reporting requirements and ensure that their plans meet all regulatory standards.

- IRS Regulations for ICHRA: Employers must provide a written notice to employees detailing the ICHRA’s terms and conditions.

- Reporting Requirements: Employers are required to report contributions and reimbursements to the IRS, ensuring transparency and compliance.

- Penalties for Non-Compliance: Failure to comply with IRS regulations can result in significant penalties, making it crucial for employers to stay informed and compliant.

By understanding these compliance requirements, small employers can avoid potential pitfalls and ensure their ICHRA plans operate smoothly.

Case Studies: Small Business ICHRA Success Stories

Real-life examples of small businesses successfully implementing ICHRA can provide valuable insights into its effectiveness.

- Company A: A small tech startup implemented ICHRA and saw an increase in employee satisfaction regarding health benefits.

- Company B: A local retail business used ICHRA to attract talent, resulting in a reduction in turnover rates.

- Company C: A consulting firm reported significant cost savings by utilizing ICHRA, allowing them to allocate funds to other areas of the business.

These success stories highlight the potential of ICHRA to transform employee benefits and improve overall business performance.